Boosted by rainfall, direct sales of snow lodges grew by 43%.

Revenue 09/04/2025

After the storm comes... the snow

With the ski season now drawing to a close, it's time to take stock. At Paraty Tech, we've thoroughly analyzed the performance of the direct channels of accommodations located in the main snow destinations on the Iberian Peninsula, focusing on three key areas: Andorra, the Pyrenees, and the Sierra Nevada .

And the results leave no room for doubt: this year's abundant rainfall , which at higher altitudes has fallen as snow, has had a very positive impact on bookings, occupancy, and revenue, especially during April, a period that last year went virtually unnoticed in terms of activity for many accommodations, which were even forced to make the decision to close their doors that month due to the lack of snow and/or the premature closure of resorts.

Below, we present the aggregated key KPIs for these three regions, and then analyze them in detail for each destination. We'll focus on metrics such as revenue, number of reservations, room nights, ADR, average stay, advance notice, cancellation rate, and booking source. We'll compare all of this with data from the previous season.

General improvement of all indicators

Before diving into a detailed analysis of each area, let's look at the overall evolution of ski accommodations during the season , according to our data. The general trend is clearly positive, and demonstrates that, despite being an increasingly exclusive product (the average ADR is around €200), skiing continues to attract a growing number of enthusiasts year after year.

The comparison between the 43.16% increase in revenue generated and the 28.35% increase in the number of reservations reveals two other very interesting indicators: on the one hand, the increase in ADR, which stands at around 10%, and on the other, the increase in Room Nights, close to 30%, with an average stay of 2.18 nights. More nights at a higher price equals more revenue, despite the lower growth in the number of reservations. Let's look at other interesting KPIs:

- Origin of the reserves:

- Spain (77.5%)

- France (16.5%)

- United Kingdom (2.3%)

- Revenue increase: +43.16%

- Increase in the number of reservations : +28.35%

- Increase in the total number of Room Nights : +29.44%

- Average stay : 2.18 nights

- ADR increase : +9.75%

- ADR : €199.61

- Average cancellation rate : -11.36% vs. last season

- Lead Time : 22.44 days

- Increase in Lead Time : +4.8 days

- Revenue increase in April : +812.48% (only hotels open both years)

Andorra: longer average stay and significant differences in ADR by market

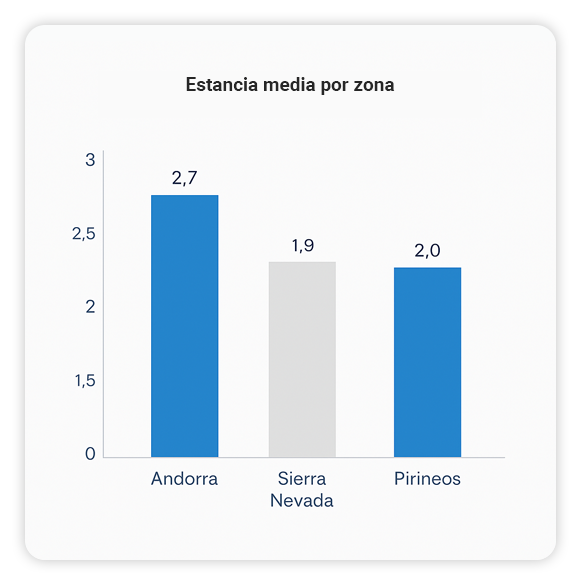

Andorra has shown more moderate growth overall, but stands out for having recorded the largest increase in revenue in April , demonstrating a significant recovery from a historically difficult period. It is also the region with the longest average stay .

The ADR in Andorra is high , although there are significant differences depending on the source market. While a French traveler can pay up to €213.90 (more than 4% above the average), a local traveler will pay close to €145 (almost 30% below the average). Below are all the details:

- Origin of the reserves:

- Spain (50.4%)

- France (24%)

- United Kingdom (6%)

- Andorra (3%)

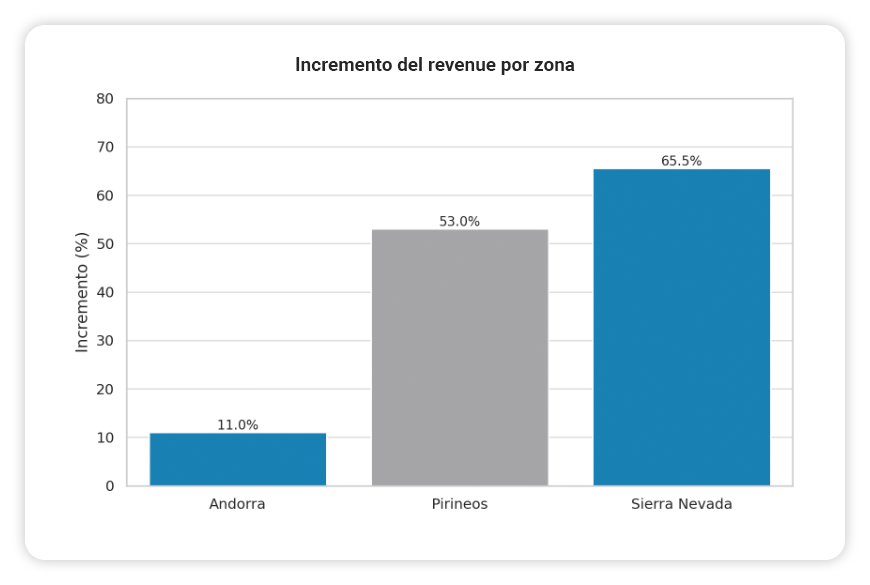

- Revenue increase : +11%

- Increase in the number of reservations : +6%

- Increase in the total number of Room Nights : +7%

- Average stay : 2.65 nights

- ADR increase : +3.5%

- ADR : €204.45

- France: €213.90 (+4.62% vs. average)

- United Kingdom: €204.90 (+0.22% vs. average)

- Spain: €200.84 (-1.76% vs. average)

- Andorra: €144.33 (-29.43% vs average)

- Cancellation rate : -23% vs. last season

- Lead Time : 25.15 days

- Increase in Lead Time : +6.25 days

- Revenue increase in April : +1098.50%

Sierra Nevada, a very popular resort

Sierra Nevada is, without a doubt, the area that has experienced the greatest growth this season. With notable increases in revenue, bookings, and room nights, in addition to a rising ADR, it reflects the popularity, predominantly among Spanish skiers (97.2% of bookings), of this southern Iberian ski resort. However, it also stands out for having the shortest average stay , a slight increase in cancellations , and hosting the least planning traveler profile (booking advance notice is just 12.97 days).

- Revenue increase : +65.50%

- Increase in the number of reservations : +42.05%

- Increase in the total number of Room Nights : +42.38%

- Average stay : 1.87 nights

- ADR increase : +14.13%

- ADR : €186.10

- Cancellation rate : +0.23%

- Lead Time : 12.97 days

- Increase in Lead Time : +2.8 days

- Revenue increase in April : +92.94%

The Pyrenees (Aragonese and Catalan) are synonymous with performance

The Pyrenees are positioned as one of the most robust regions in terms of performance. They have experienced significant growth across all KPIs, with a high ADR, excellent performance in April, and very low cancellation rates . Furthermore, it is the region with the highest average advance booking rate.

- Origin of the reserves:

- Spain (91%)

- France (6.2%)

- United Kingdom (1.5%)

- Revenue increase : +53%

- Increase in the number of reservations : +37.06%

- Increase in the total number of Room Nights : +38.95%

- Average stay : 2.02 nights

- ADR increase : +11.63%

- ADR : €208.28

- Cancellation rate : -11.33%

- Lead Time : 29.22 days

- Increase in Lead Time : +5.4 days

- Revenue increase in April : +1246%

With the weather permitting, skiing will continue to be fashionable, no matter the cost.

Andorra leads in average stays, the Pyrenees in advance, and the Sierra Nevada in booking growth . These and the rest of the data presented confirm that the 2024-2025 snow season has been very positive for mountain accommodations, thanks in large part to the generous snowfall recorded, which has allowed many resorts to extend operations into April.

But also because, despite the fact that skiing remains an expensive product— with an average ADR approaching €200 per night —demand remains strong, and the overall improvement in indicators supports this.

In fact, it is increasingly attracting young people, and its new followers continue to grow, attracted not only by the improvements in the facilities, such as the addition of snow parks, but also by that other fun aspect associated with this sport known as après-ski .

With a wide variety of events and concerts taking place at the resorts, sometimes even on the slopes themselves, a multitude of championships being held (freestyle, slalom, etc.), and countless complementary activities (guided snowshoe tours, sleigh rides, snow grooming, etc.), the door is also opening up to developing dynamic packages in this segment, whose contribution to increasing direct sales and the average ticket is already very significant for many of our clients.

It's time to take advantage of the last moments of the season! We recommend checking the current status of the slopes, the expected closing date for each resort, and other details relevant to your business. You can do so at Infonieve . However, for your convenience, below is a list of the resorts that plan to close at the end of April:

- April 20, 2025

- Panticosa

- Nuria Valley

- Astún

- Candanchú

- Cerler

- Formigal

- San Isidro

- Laciana Valley - Leitariegos

- Winter Fountains

- Ordino Arcalís

- Pal Arinsal

- Grandvalira

- April 21, 2025

- Piau-Engaly

- Vallter

- Cauterets Cirque du Lys

- Spot

- The Molina

- Port Ainé

- Baqueira Beret

- Ski Canaro

- Boí Taüll

- April 27, 2025

- Masella

- May 5, 2025

- Sierra Nevada