Winter 2026: year-on-year growth with slowing and greater volatility in hotel demand

Revenue 13/02/2026

The winter of 2026 is creating a complex scenario for the hotel sector in various Spanish urban destinations. In addition to adverse weather conditions, there is an environment of uncertainty surrounding rail travel following recent incidents and service disruptions.

Several surveys published in recent weeks reflect a decline in user confidence in trains as a means of transport. Beyond this stated perception, the relevant question is whether this situation is having a tangible impact on hotel occupancy data.

To answer this question, at Paraty Tech we have analyzed, based on our direct sales data, the year-on-year evolution of the pickup truck, focusing on:

The study focuses on Cádiz, Málaga, Seville, Córdoba, and Madrid. The selection is based on exposure to rail connectivity, especially along the Madrid-Andalusia axis.

These are destinations with a significant domestic market share and short and medium stay trips, segments that are potentially more sensitive to changes in the perception of transport reliability.

Madrid also serves a dual purpose: it is a well-established urban destination and the main hub for sending tourists to and connecting with the southern Iberian Peninsula. This allows us to observe the behavior of both the source market and the receiving destinations.

Our goal is not to extrapolate conclusions to the whole of the country, but to analyze those markets where, according to the sample we manage, a change in mobility could have a greater impact.

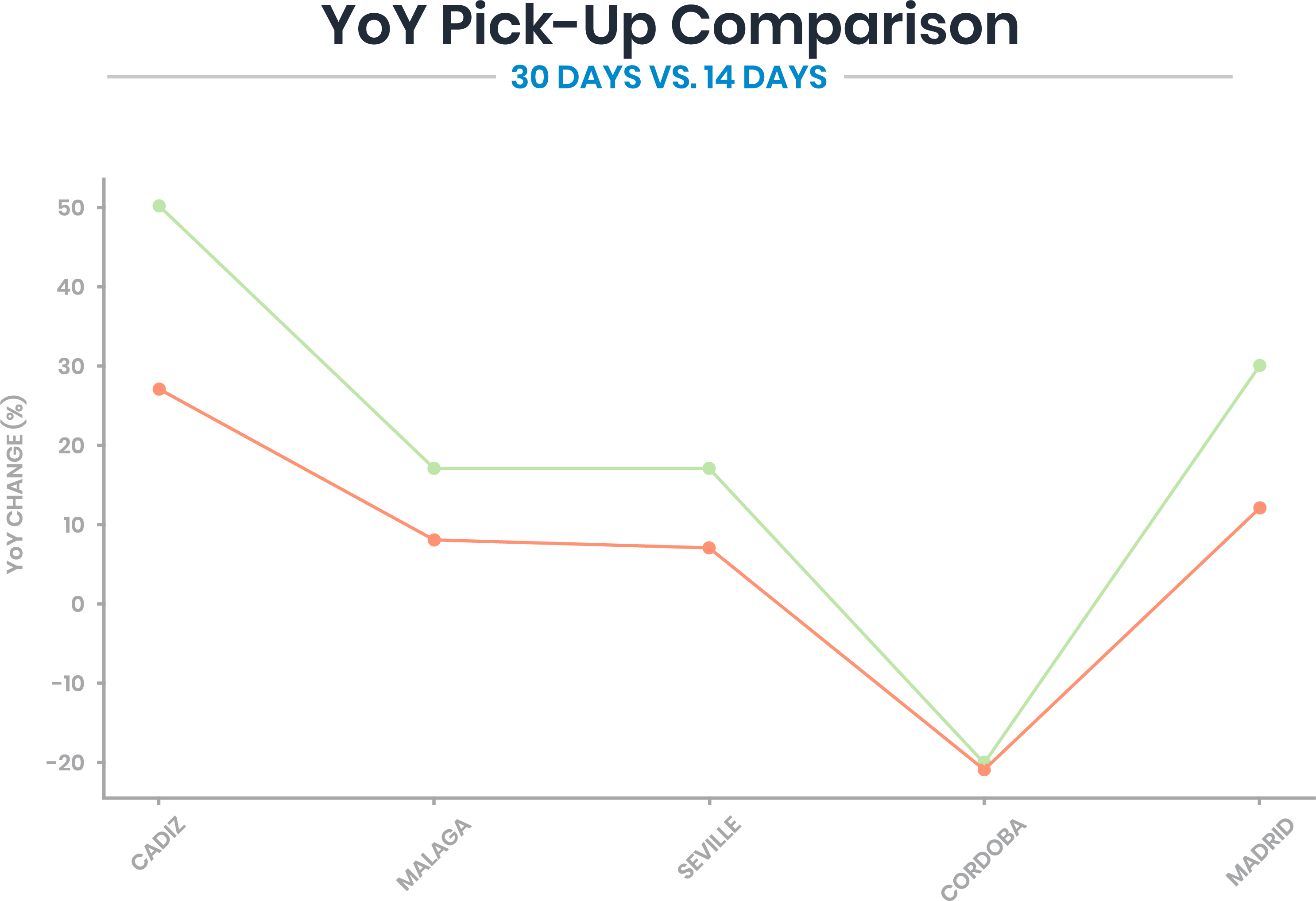

According to the data we have, the pattern is consistent across the five destinations: the year-on-year growth rate is lower in the last 14 days than in the last 30.

The YoY pickup chart visually shows this lateral deceleration.

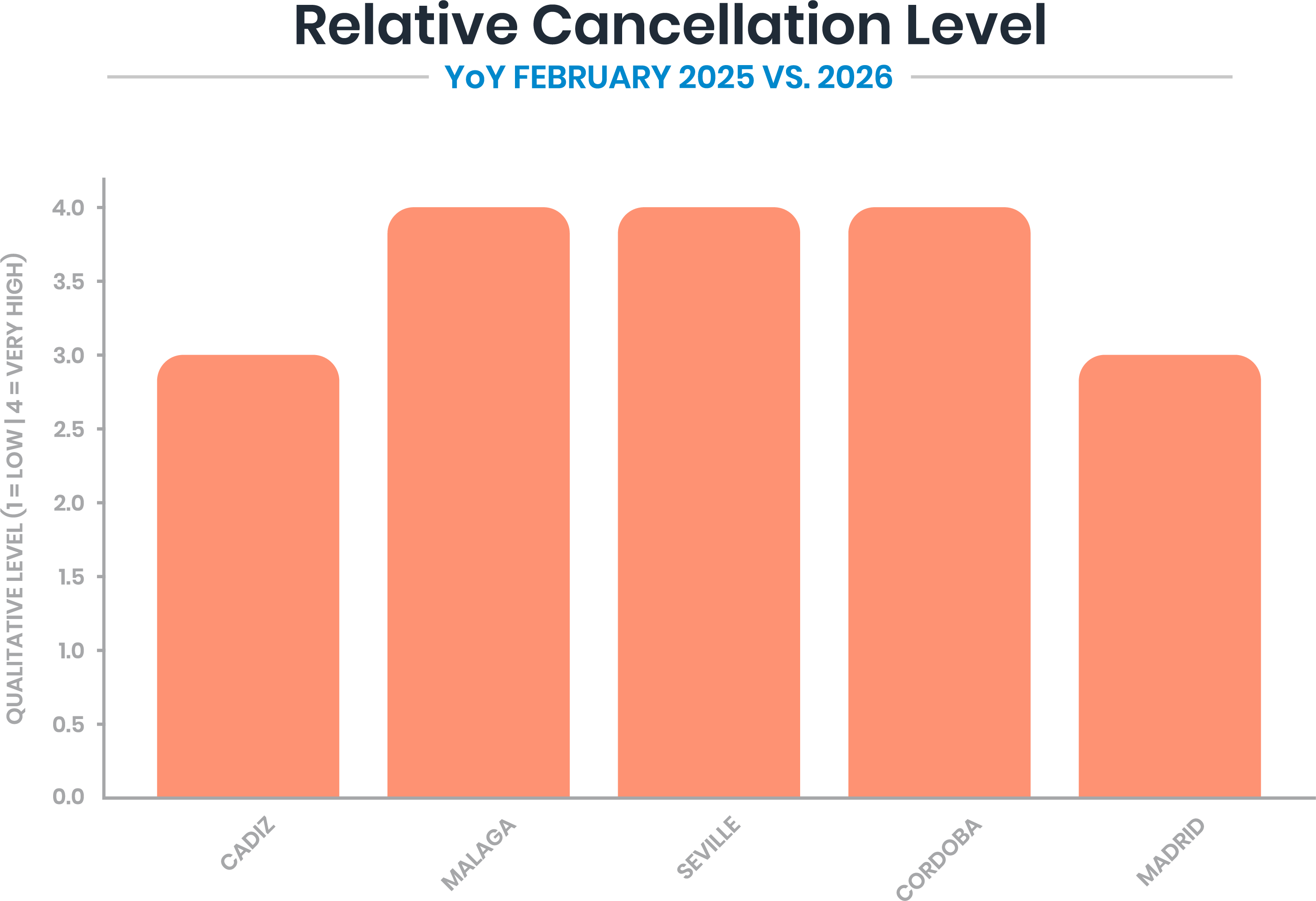

If we apply the same comparative analysis to the year-over-year behavior of cancellations, the pattern is consistent again: February shows the largest year-over-year difference in most destinations.

According to the data we have, the breakdown by location would be as follows:

From a purely technical perspective, the combined effect is clear:

Another relevant pattern is the concentration of cancellations in February. This is observed in several destinations:

According to the data we have at Paraty Tech, winter 2026 does not reflect a widespread contraction in year-over-year growth in the destinations analyzed. Four of the five locations maintain positive year-over-year variations in revenue and pick-up.

However, comparative analysis between time windows reveals a consistent pattern of slowdown in the last 14 days compared to the previous 30, accompanied in several cases by a relative increase in cancellations.

From an analytical perspective, this behavior suggests:

Beyond the current analysis, the data points to an environment where the critical variable is not only the pace of sales, but also the stability of the reserve. In a context of greater volatility:

Continuous monitoring of the relationship between revenue generated and consolidated revenue will be crucial in the coming weeks.

Several surveys published in recent weeks reflect a decline in user confidence in trains as a means of transport. Beyond this stated perception, the relevant question is whether this situation is having a tangible impact on hotel occupancy data.

To answer this question, at Paraty Tech we have analyzed, based on our direct sales data, the year-on-year evolution of the pickup truck, focusing on:

- Last 30 days

- Last 14 days

- Year-over-year comparison of revenue and cancellations

Delimitation of the analysis: why these destinations

The study focuses on Cádiz, Málaga, Seville, Córdoba, and Madrid. The selection is based on exposure to rail connectivity, especially along the Madrid-Andalusia axis.

These are destinations with a significant domestic market share and short and medium stay trips, segments that are potentially more sensitive to changes in the perception of transport reliability.

Madrid also serves a dual purpose: it is a well-established urban destination and the main hub for sending tourists to and connecting with the southern Iberian Peninsula. This allows us to observe the behavior of both the source market and the receiving destinations.

Our goal is not to extrapolate conclusions to the whole of the country, but to analyze those markets where, according to the sample we manage, a change in mobility could have a greater impact.

Generalized deceleration in the short window

According to the data we have, the pattern is consistent across the five destinations: the year-on-year growth rate is lower in the last 14 days than in the last 30.

- Cadiz: +50% → +27%

- Malaga: +17% → +8%

- Seville: +17% → +7%

- Madrid: +30% → +12%

- Cordoba: -20% → -21%

The YoY pickup chart visually shows this lateral deceleration.

Increased volatility: the growing weight of cancellations

If we apply the same comparative analysis to the year-over-year behavior of cancellations, the pattern is consistent again: February shows the largest year-over-year difference in most destinations.

According to the data we have, the breakdown by location would be as follows:

- Cadiz : notable year-on-year increase in February, with gradual normalization in the following months.

- Malaga : one of the highest relative peaks in cancellations during the period, especially concentrated in February.

- Seville : significant increase in cancellations at the start of the year, coinciding with the adjustment observed in the short window.

- Madrid : year-on-year revenue growth accompanied by a high level of cancellations in February, which reinforces the idea of greater volatility.

- Cordoba : significant increase in cancellations in February within an already contractionary context in customer acquisition.

From a purely technical perspective, the combined effect is clear:

- Less inertia in recent capture.

- Higher probability of reserve reversal.

- Reduction of net visibility in the very short term.

February is the month with the highest tension

Another relevant pattern is the concentration of cancellations in February. This is observed in several destinations:

- Significant year-on-year increase in cancellations.

- Notable differences between revenue growth and booking stability.

- A key event in Cádiz: Carnival. This demand will not be postponed to a future date.

- The cancellation chart reinforces this reading: the relative level of cancellations in February is high in virtually all destinations analyzed.

- The observed behavior does not point to a disappearance of demand, but rather to greater volatility. Reservations are being made, but cancellations are also occurring more frequently than last year.

Technical conclusion

According to the data we have at Paraty Tech, winter 2026 does not reflect a widespread contraction in year-over-year growth in the destinations analyzed. Four of the five locations maintain positive year-over-year variations in revenue and pick-up.

However, comparative analysis between time windows reveals a consistent pattern of slowdown in the last 14 days compared to the previous 30, accompanied in several cases by a relative increase in cancellations.

From an analytical perspective, this behavior suggests:

- Loss of inertia in recent capture.

- Greater volatility in reserve consolidation.

- Concentration of risk in certain months, especially February.

- The market, therefore, does not show a structural drop in interest in destinations, but rather a deterioration in the stability of demand in the very short term.

Implications for revenue management

Beyond the current analysis, the data points to an environment where the critical variable is not only the pace of sales, but also the stability of the reserve. In a context of greater volatility:

- The 14-day window becomes more relevant as a leading indicator.

- Managing cancellation policies and flexible terms is of particular importance.

- Net pick up analysis (bookings minus cancellations) becomes a key metric.

Continuous monitoring of the relationship between revenue generated and consolidated revenue will be crucial in the coming weeks.